Cutler Commentary

Market and Equity Income Commentary 2Q 2018

July 10, 2018

Cutler’s Equity Income strategy uses a dividend-based criteria approach for managing large capitalization equities. The strategy is most memorably known for our “10-years of dividend payments without a cut” screen; a screen which dates back to Ken Cutler’s equity research upon which he founded the strategy in the late 1970’s.

The resulting portfolio is comprised of high-quality companies with long dividend histories. We have a value bias, always looking at relative valuations in order to identify investment opportunities. In our view, this portfolio is a cross-section of blue chip US companies, all of whom can stand alone as a defensible investment within client portfolios.

We continue to manage portfolios in this manner, in order to achieve our philosophical goals of income, lower risk, and total return. We believe these three goals are interconnected and that any one can positively contribute to achieving the others. In a market where growth has outperformed value by significant margins, we believe that conviction to our process is essential in today’s market with such “high flying momentum” stocks.

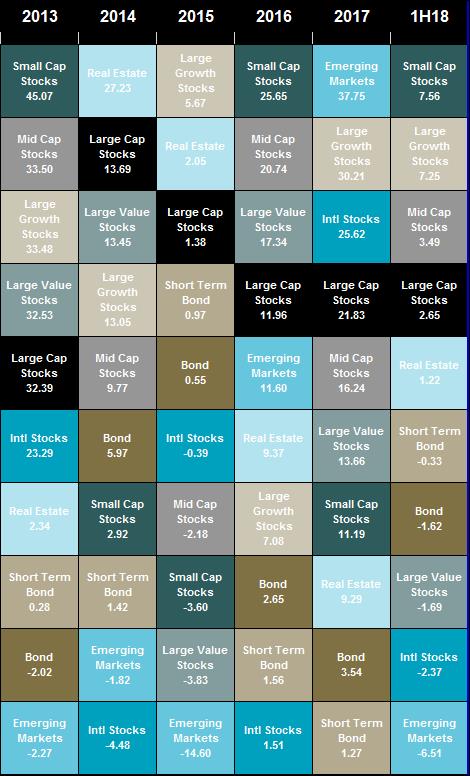

As an example of this market dispersion, consider the chart to the left. This chart shows the performance of various asset classes for the previous five years, as well as for the first half of 2018. Notably, small cap stocks and large cap growth outperformed considerably so far this year. This can be attributed to insulation from trade disputes (for small cap) and a continuation of the secular outperformance of big tech (for large cap growth). If you would like this chart as a separate document with additional historical data, please contact your representative at Cutler.

Our Equity Income portfolio composite had a gross return of 1.23% (1.04% net) during the quarter. This compares favorably to the Russell 1000 Value index, which had a return of 1.18% in the same period. Perhaps surprisingly, Kroger was the single best performing security in the quarter up 19%. Kroger has been much maligned since the Amazon purchase of Whole Foods last year. While the combination of Whole Foods and Amazon remains a considerable threat, our patience with Kroger has been rewarded. The company continues to have a very strong presence throughout the country and remains a formidable competitor to Whole Foods as well as portfolio holding WalMart.

Kroger is an interesting contrast to General Mills, which was sold during the quarter. Our investment team felt that the lack of pricing power from General Mills made a long-term recovery less likely and chose to exit this position in favor of Medtronic. Medtronic is a leader in the medical device field, a company with which we believe there are favorable demographic trends as well as a high barrier to entry for competitors.

In addition to Medtronic, Union Pacific was added to the strategy during the quarter. Similar to the comments above, it is very difficult to establish a new railroad today. Union Pacific has a strong market position and as a domestic company is not directly involved in trade disputes.

Finally, Energy was a standout performer during the period. Both Exxon and Chevron had gains of 11.98% and 11.85% respectively. Given the rally in oil prices globally, this strong quarter is not surprising, and is discussed further in our commentary below. A sustained rally in energy companies will require global growth to continue its expansion to maintain the current demand for the commodity.

Second Quarter Market Commentary

The second quarter experienced further volatility in both stocks and bonds, as investors continued to digest and interpret news ranging from interest rate increases to trade wars to earnings results. Despite enduring more volatile trading days, the major domestic stock indexes provided positive results for the quarter- with the S&P 500 index gaining 3.4% for the period. This is still below the 5.7% gain for that index in January alone, but is a solid recovery from the slightly negative total return endured for the first quarter after sharp drops in both February and March.

The quarter showed significant disparity in returns by sector, but the winners and losers had some changes versus the first quarter. Gains were led for the quarter by the Energy sector, with a return of over 12%, as oil climbed back to over $70 a barrel on talks of supply constrictions and some increased global demand. This impact of oil price gains can be seen in the disparity between two key commodity index returns: the S&P GSCI index, with over 50% allocated to energy, has gained over 10% this year to date, while the Bloomberg Commodity Index, with 1/3 allocated to energy, ended the second quarter completely flat year to date. The next highest gains were in Technology and Consumer Discretionary sectors. Both are Growth-style sectors that have widely paced multi-year returns (see asset class chart above), but which are also currently quite stretched on average valuations.

Meanwhile, non-domestic stock indexes continued to struggle this year, with the MSCI EAFE index down about 1% for the quarter and down 2.8% for the year to date, and the MSCI Emerging Markets index down almost 8% for the quarter alone to bring down the year to date return to a drop of more than 6.5%. These classes have been hit by a variety of issues, such as key elections, tariffs and trade war concerns with the U.S., plus the ongoing relative strength of the dollar and impact that has on dollar-adjusted total returns.

Please reach out to us if you have questions about the markets and how they can impact your portfolio holdings.

Past performance is no guarantee of future results. Net performance is pre-tax, net of advisory fees and transaction costs and includes the reinvestment of dividends. All investments involve risk, including possible loss of principal amount invested. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be profitable or suitable for a particular investor's financial situation or risk tolerance. Asset allocation and portfolio diversification cannot assure or guarantee better performance and cannot eliminate the risk of investment losses. Source: Morningstar

All opinions and data included in this commentary are as of July 10, 2018 and are subject to change. The opinions and views expressed herein are of Cutler Investment Counsel, LLC and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This report is provided for informational purposes only and should not be considered a recommendation or solicitation to purchase securities. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither Cutler Investment Counsel, LLC nor its information providers are responsible for any damages or losses arising from any use of this information.

TOP 5 AND BOTTOM 5 HOLDINGS BY PERFORMANCE - AS OF 6.30.18 |

||

Best Performing Securities |

Average Weight (%) |

Security Contribution to Portfolio Return (%) |

The Kroger Co. |

1.99 |

0.38 |

Merck & Co. Inc. |

2.38 |

0.28 |

Exxon Mobil Corp. |

2.51 |

0.29 |

Chevron Corp. |

3.50 |

0.40 |

Becton, Dickinson and Co. |

4.08 |

0.44 |

|

|

|

|

Worst Performing Securities |

Average Weight (%) |

Security Contribution to Portfolio Return (%) |

Bristol-Myers Squibb Company |

2.73 |

-0.38 |

Deere & Co. |

4.43 |

-0.45 |

Prudential Financial Inc. |

2.42 |

-0.22 |

AT&T Inc. |

2.36 |

-0.22 |

Caterpillar Inc. |

4.24 |

-0.32 |

For Historical Returns Chart:

Large Cap Stocks are represented by the Standard & Poors (S&P) 500 Index. Large Value Stocks are represented by the Russell 1000 value index. Large Growth Stocks are represented by the Russell 1000 growth index. Mid Cap Stocks are represented by the Standard & Poors (S&P) MidCap 400 Index. Small Cap Stocks are represented by the Ibbotson and Associates Small Stock Index. International Stocks are represented by the MSCI EAFE Index. Emerging Markets Stocks are represented by the MSCI EM Index. Real Estate is represented by the FTSE NAREIT US Real Estate Index. Bonds are represented by the Barclays Capital Aggregate Bond Index. Short Term Bonds are represented by the Barclays Capital Government/Credit 1-5 Year Index. An investment cannot be made directly into an index.

CATEGORIES

Disclaimer

These blogs are provided for informational purposes only and represent Cutler Investment Group’s (“Cutler”) views as of the date of posting. Such views are subject to change at any point without notice. The information in the blogs should not be considered investment advice or a recommendation to buy or sell any types of securities. Some of the information provided has been obtained from third party sources believed to be reliable but such information is not guaranteed. Cutler has not taken into account the investment objectives, financial situation or particular needs of any individual investor. There is a risk of loss from an investment in securities, including the risk of loss of principal. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable or suitable for a particular investor's financial situation or risk tolerance. Any forward looking statements or forecasts are based on assumptions and actual results are expected to vary. No reliance should be placed on, and no guarantee should be assumed from, any such statements or forecasts when making any investment decision.