Cutler Commentary

Equity Income 3Q 2017

October 18, 2017

Cutler’s Q3 2017 Market Commentary

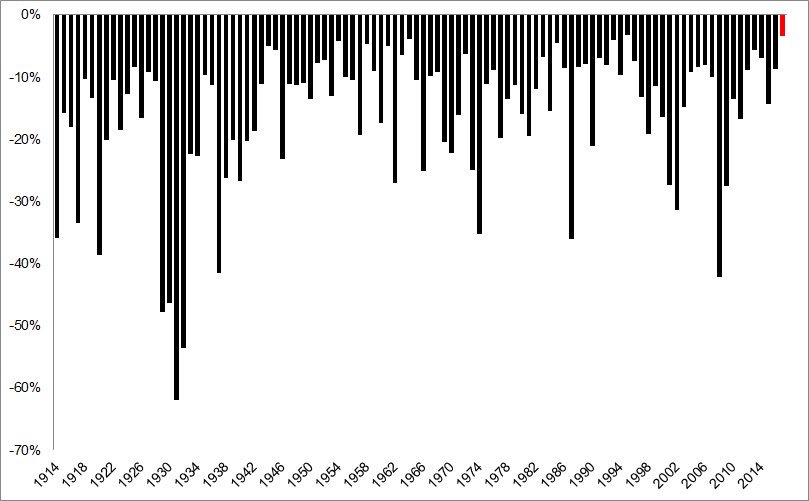

This has been an extraordinary market in a number of ways. Resilient. Optimistic. Growth. Investors have benefitted from a coordinated global expansion that has resulted in equity market gains around the globe. Remarkably, these gains have come with little “pain”, as stocks have hardly had a misstep thus far in 2017. In fact, when looking at the drawdown of stocks, this has been the least volatile year in history thus far. Take a look at the chart below.

Not surprisingly, the VIX Volatility Index has been at historic lows this year. As such, investors have been enjoying all of the upside, without any of the downside! The S&P 500 TR through September 30th, was up 14.24%. And, it was up 4.48% in the 3rd Quarter alone. Investors who “sold in May and went away” this year, left quite a bit on the table. In fact, this continued bull market has had positive returns for 18 of the past 19 quarters!

While positive returns are what investors look for, astute investors are consistently asking “What’s next?” There has been a great deal of commentary about market valuations. By several measures, stocks look very expensive. We believe that investors should be aware of valuations, but not beholden to them. Warren Buffett recently commented on CNBC, that “Stock valuations make sense with interest rates where they are.” His comments imply that a lower “equity risk premium” is acceptable, because the return potential from bonds are so low. Worth noting is that Mr. Buffett’s company is holding about $100 billion in cash, so he must not think all stocks are a screaming bargain.

Conversely, Janet Yellen, Chair of the Federal Reserve, believes a tight labor market will lead to inflation pressure and that interest rates need to rise. If the Chairwoman is correct about inflation, that development would present a risk to equity market investors. Thus far, however, Federal Funds rate increases have not translated into increased inflation expectations or higher rates in the long-term. In fact, the predominant theme in 2017 has been a flattening curve, traditionally not a great indication of economic strength. Equity investors should keep a close eye on this trend. A steeper curve could be beneficial for financial stocks, as well as an indication of underlying growth.

Equity Income Update:

Cutler’s Equity Income strategy performed roughly even with the market in the 3rd-Quarter, with a return of 4.33% (gross) and 4.18% (net) versus the S&P 500 TR return of 4.48%. This was welcome performance after such strong outperformance of growth versus value in the first half of the year. Cutler took steps in the 3rd Quarter to reduce consumer exposure, selling Target and replacing it with Marsh & McLellan. Target’s exposure to the online trend, primarily Amazon.com, has been well-documented and the stock price has reflected the shift to online retailing. However, the stock had performed very well recently, up about 14% in the quarter. Cutler took advantage of this recovery to sell the position and buy a company in the insurance brokerage business. “Marsh Mac” is not an underwriter of insurance policies, so has no direct exposure to the recent plethora or disasters that have seemed all too common of late. The company has a very large “moat”, an industry term implying difficult barriers for new competitors. As a $46 billion market capitalization company with over 60,000 employees, MMC very much fits the profile of stability that Cutler looks for in our portfolio holdings.

A quick round-up of the best and worst performing sectors yields a few surprises based on recent market trends. Technology once again led the market higher, up 8.62%. But, Energy, which has been a laggard was the next best performing sector up 6.84%. Utilities benefitted from the flattening yield curve mentioned above, and rallied 6.79%.

The only S&P 500 sector negative for the quarter was Consumer Staples, down 1.87%. Consumer behavior seems to be rapidly evolving, with today’s consumers less focused on “brands” and more focused on factors such as price, environmental footprint, and individualism. The changing consumer was very much a consideration in the recent proxy battle between portfolio holding P&G and Nelson Peltz, who was seeking to gain a board seat. While Mr. Peltz was ultimately defeated, consumer goods companies will need to evolve more rapidly than ever before.

Cutler continues to manage our Equity Income portfolio consistent with our historical process. While the defensive characteristics of dividend investing may not be widely appreciated in a period of historically low volatility, we believe patient investors are rewarded for their consistency of thought and process. We continue to advocate for equity market participation through well-established, dividend paying companies.

All opinions and data included in this commentary are as of October 16, 2017 and are subject to change. The opinions and views expresses herein are of Cutler Investment Counsel, LLC and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This report is provided for informational purposes only and should not be considered a recommendation or solicitation to purchase securities. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither Cutler Investment Counsel, LLC nor its information providers are responsible for any damages or losses arising from any use of this information.

The S&P 500® Index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 7.8 trillion benchmarked to the index, with index assets comprising approximately USD 2.2 trillion of this total. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization. This index is not available for direct investment.

| TOP 5 AND BOTTOM 5 HOLDINGS BY PERFORMANCE - AS OF 9.30.17 | ||

| Best Performing Securities | Average Weight (%) | Security Contribution to Portfolio Return (%) |

| Texas Instruments Inc. | 4.00 | 0.68 |

| Caterpillar Inc. | 3.44 | 0.57 |

| Bristol-Myers Squibb Company | 2.97 | 0.45 |

| Target Corp. | 2.16 | 0.30 |

| Chevron Corp. | 3.28 | 0.45 |

| Worst Performing Securities | Average Weight (%) | Security Contribution to Portfolio Return (%) |

| The Kroger Co. | 2.00 | -0.28 |

| Walt Disney Co. | 3.63 | -0.24 |

| General Mills Inc. | 2.40 | -0.14 |

| Qualcomm Inc. | 2.09 | -0.11 |

| Northern Trust Corp. | 2.49 | -0.13 |

The performance information shown above has been calculated using the composite managed by the firm in the Equity Income strategy. Information on the methodology used to calculate the performance information and a list reflecting the contribution of all the holdings in the composite to the composite's overall performance during the time period reflected above, is available upon request.

Holdings are subject to change. Cutler Investment Counsel, LLC or one or more of its officers, may have a position in the securities discussed herein and may purchase or sell such securities from time to time.

CATEGORIES

Disclaimer

These blogs are provided for informational purposes only and represent Cutler Investment Group’s (“Cutler”) views as of the date of posting. Such views are subject to change at any point without notice. The information in the blogs should not be considered investment advice or a recommendation to buy or sell any types of securities. Some of the information provided has been obtained from third party sources believed to be reliable but such information is not guaranteed. Cutler has not taken into account the investment objectives, financial situation or particular needs of any individual investor. There is a risk of loss from an investment in securities, including the risk of loss of principal. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable or suitable for a particular investor's financial situation or risk tolerance. Any forward looking statements or forecasts are based on assumptions and actual results are expected to vary. No reliance should be placed on, and no guarantee should be assumed from, any such statements or forecasts when making any investment decision.