Cutler Commentary

Equity Income 4Q 2017

January 11, 2018

Cutler 2018 Market Outlook

Wow! What a year 2017 was for investors. It was, quite literally, an historic one. For the first time ever, the S&P 500 did not have a negative month. Volatility hit all-time low levels. The market, as of this writing, still has not had a 3% correction since the 2016 election. The S&P 500 TR finished the year up 22.23%, exceeding the expectations of even the most optimistic prognostications.

The market often correctly anticipates economic conditions. Years like 2017 are only possible when the economy exceeds expectations, which has happened as of late. Furthermore, the tax reform passed at the end of the year was largely supportive of stock prices. Lower corporate tax rates are a direct benefit to the earnings of publicly traded companies. The S&P 500’s lofty valuation became more sensible once the new policy had passed.

Note the caution in that last sentence, however. “Lofty valuation” is not an expression that brings comfort to investors. After all, by certain measures (such as the Schiller CAPE Cyclically Adjusted Price/Earnings ratio) stocks are the 3rd priciest in history. By other measures, such as a traditional Forward Price/Earnings ratio, valuations are more reasonable but still expensive. The S&P 500 forward P/E is currently 18.2x versus the 25-year average of 16x. Why? First, interest rates have stayed low. The yield curve flattened in 2017, as the Federal Reserve raised short-term rates and long-term rates did not rise. Another reason stocks are expensive? They are anticipating growth. If the economy is accelerating, this is a reasonable expectation. If, however, inflation increases and rates rise, be wary. This may be the possible catalyst for stock valuations to return to a normalized level.

Note the caution in that last sentence, however. “Lofty valuation” is not an expression that brings comfort to investors. After all, by certain measures (such as the Schiller CAPE Cyclically Adjusted Price/Earnings ratio) stocks are the 3rd priciest in history. By other measures, such as a traditional Forward Price/Earnings ratio, valuations are more reasonable but still expensive. The S&P 500 forward P/E is currently 18.2x versus the 25-year average of 16x. Why? First, interest rates have stayed low. The yield curve flattened in 2017, as the Federal Reserve raised short-term rates and long-term rates did not rise. Another reason stocks are expensive? They are anticipating growth. If the economy is accelerating, this is a reasonable expectation. If, however, inflation increases and rates rise, be wary. This may be the possible catalyst for stock valuations to return to a normalized level.

What to expect from here?

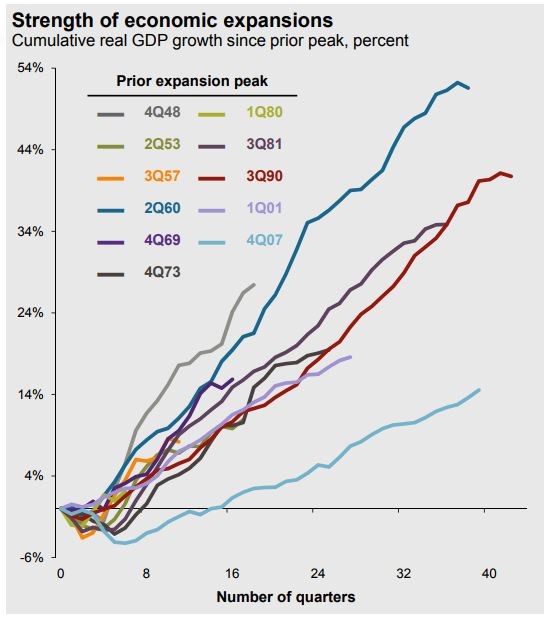

The best argument for stocks to go down, is that they have gone up so significantly. The current recovery, however, while it has been long, has not been strong (see the chart nearby from JP Morgan through 12/31/2017). It is plausible that the economy is still catching up, and stocks can also drift higher.

While this is a plausible outcome, we are still recommending reducing risk. Growth and momentum have dominated index performance. Should we see a return of market volatility, value stocks may once again return to favor. We would be positioning equity portfolios in anticipation of potential volatility heading into 2018.

Equity Income Strategy Update Q4-17

Cutler’s Equity Income strategy focuses on dividend paying stocks. These are typically well-established companies, often with stable cash flows, and significant capital investments. This last point is crucial when looking at the fourth quarter stock market, as capital-intensive industries were targeted to benefit the most by the recent tax reform. Portfolio holdings Caterpillar (up 27% in Q4) and Deere (up 25% in Q4) are examples of companies well positioned for changes to the current law. Other strong performers during the quarter were Kroger (up 37%) and Qualcomm (up 24%), which were both “beaten down” stocks in the portfolio. Qualcomm received an unsolicited take-over bid from Broadcom, which has set up a proxy battle for 2018.

The bottom-performing stocks in the strategy were led by health care. Merck (down 11%) and Bristol-Myers (down 3%) were the two biggest drags on the portfolio, followed by Schlumberger (down 2%), new holding MarshMac (down 2%), and National Fuel Gas (down 2%).

Overall, the fourth quarter was very strong. Cutler’s Equity Income strategy finished the fourth quarter up 10.24% (gross) and 10.10% (net) versus the S&P 500 TR of 6.64%. This was a very nice Christmas present for Cutler clients. We believe that the strategy continues to be positioned well for today’s investors. We are looking for valuation opportunities where the market provides them, always with an eye on the appropriate level of portfolio risk.

Past performance is no guarantee of future results. Net performance is pre-tax, net of advisory fees and transaction costs and includes the reinvestment of dividends. All investments involve risk, including possible loss of principal amount invested. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be profitable or suitable for a particular investor's financial situation or risk tolerance. Asset allocation and portfolio diversification cannot assure or guarantee better performance and cannot eliminate the risk of investment losses. Source: Morningstar, Advent APX, and Cutler Investment Group.

All opinions and data included in this commentary are as of January 9, 2018, and are subject to change. The opinions and views expresses herein are of Cutler Investment Counsel, LLC and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This report is provided for informational purposes only and should not be considered a recommendation or solicitation to purchase securities. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither Cutler Investment Counsel, LLC nor its information providers are responsible for any damages or losses arising from any use of this information.

The S&P 500® Index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 7.8 trillion benchmarked to the index, with index assets comprising approximately USD 2.2 trillion of this total. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization. This index is not available for direct investment.

The performance information shown above has been calculated using the composite managed by the firm in the Equity Income strategy. Information on the methodology used to calculate the performance information and a list reflecting the contribution of all the holdings in the composite to the composite's overall performance during the time period reflected above, is available upon request.

Holdings are subject to change. Cutler Investment Counsel, LLC or one or more of its officers, may have a position in the securities discussed herein and may purchase or sell such securities from time to time.

CATEGORIES

Disclaimer

These blogs are provided for informational purposes only and represent Cutler Investment Group’s (“Cutler”) views as of the date of posting. Such views are subject to change at any point without notice. The information in the blogs should not be considered investment advice or a recommendation to buy or sell any types of securities. Some of the information provided has been obtained from third party sources believed to be reliable but such information is not guaranteed. Cutler has not taken into account the investment objectives, financial situation or particular needs of any individual investor. There is a risk of loss from an investment in securities, including the risk of loss of principal. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable or suitable for a particular investor's financial situation or risk tolerance. Any forward looking statements or forecasts are based on assumptions and actual results are expected to vary. No reliance should be placed on, and no guarantee should be assumed from, any such statements or forecasts when making any investment decision.