Cutler Commentary

Cutler’s 3rd Quarter Commentary and Market Outlook

October 13, 2025

“The future is not set. There is no fate but what we make for ourselves.” — Sarah Connor, The Terminator

What is Artificial Intelligence? The field was founded in the 1950’s by Dartmouth professor John McCarthy. Known as the “father of AI,” he coined the term “Artificial Intelligence” and held the belief that “every aspect of intelligence can, in principle, be simulated by a machine.” In short, he envisioned “sentient” machines capable of thinking and reasoning like a human. The path for AI has taken an interesting detour from McCarthy’s vision to today’s Large Language Models (LLM), which are trained on enormous datasets. Modern LLMs rely on these massive, centralized datasets to generate language patterns, but they do so without true understanding or human-like reasoning. LLMs are like a fancier Google Search: they’ve read mammoth amounts of text and can generate responses that sound knowledgeable, but unlike a search engine, they don’t retrieve exact sources or truly understand the meaning. They simply predict what words are likely to come next.

When it comes to AI, Wall Street is betting big on what is “likely to come next.” The evolution of LLMs, from “text predictors” to “reasoning systems” (LLMs solving problems) to “multi-model agents” (applying different inputs such as text and audio and translating to real-world actions like robotic movement) to “goal directed AI” represent the fuller completion of McCarthy’s vision to replicate human actions using machines. Each of these breakthroughs represents a huge leap forward, with immense risks for failure – or worse, gasp, an inability to monetize the technological advancement. Yet, the time for capital investment is clearly now.

We are in the midst of the largest capital investment “arms race” in history. The largest companies in history are investing the largest sums in history, to advance their own AI ecosystems. It is estimated that in 2025, $414 Billion will be spent by the Magnificent 7 companies on datacenters and AI infrastructure. Is $414 Billion a difficult number to visualize? Yes. Perhaps it is easier to understand the recent hiring of Matt Dietke at Meta (Facebook). Recently a PhD student at the University of Washington, the 24-year-old had co-founded an AI startup and worked on multimodel AI projects. It is rumored that Mark Zuckerberg offered him a $250 million pay package to join Meta’s Superintelligence Lab (only after refusing $125 million initially). The numbers being thrown about are staggering. And the stock market has taken notice.

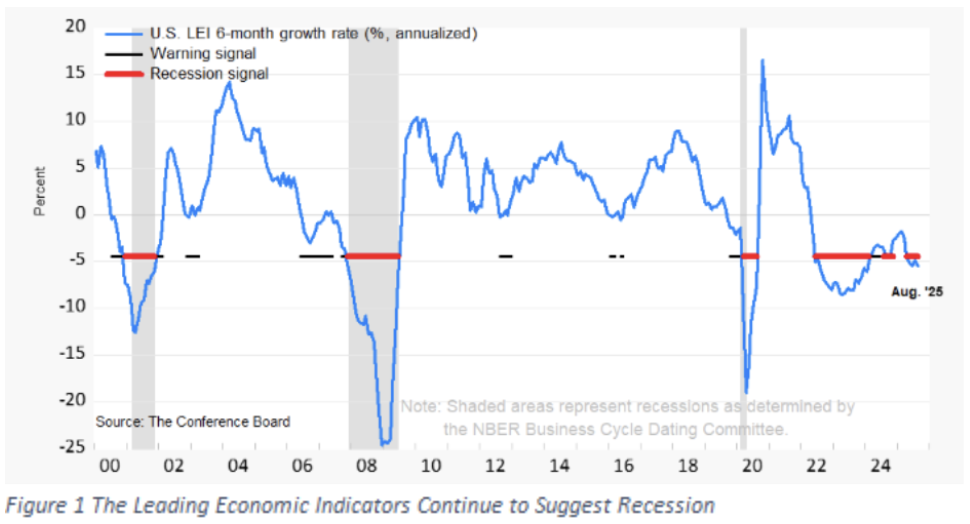

Since ChatGPT launched 35 months ago (on November 30th, 2022), the S&P 500 has a return (including dividends) greater than 70%. Yet for most of the past 36 months, the Leading Economic Indicators index has suggested that the economy has had an elevated risk of recession (see the following chart).

The disconnect? Despite various theories, the explanation seems quite obvious. The investment in AI has bolstered the economy and staved off negative growth. With the $414 billion of estimated AI investment this year, it is no wonder we maintain positive economic GDP growth.

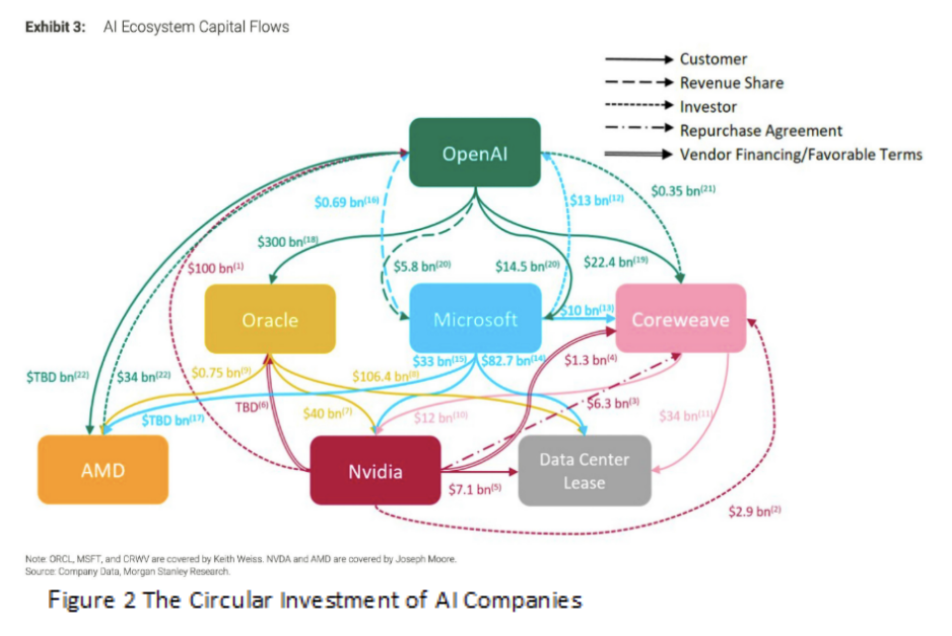

The beauty of the American economy is that we are not spectators to this revolution. In fact, we are active participants through the deployment of capital. We can choose where to invest based on where we believe the greatest return on our investment lies for the future. Thus far, gains have been concentrated at the top of the S&P 500. NVIDIA has been the AI bellwether, rocketing to the top of the market and a $4.5 Trillion valuation. Unlike in the past with tulips in Holland or Pets.com in 1999, this rally has been supported by earnings growth. In January 2023, NVIDIA posted earnings of $0.76/share. By July of this year, that figure had grown to an astronomical $3.54/share! Semi-conductor stocks like NVIDIA have been the largest beneficiaries from the “hyperscalers,” the term for the tech firms building out their LLM infrastructure. As investors continue to deploy capital, the questions must be asked, “Will the AI buildout end with a bust? Will the circular investment cycle, where companies continue to invest in each other, result in a game of musical chairs when the music stops?” The nearby chart helps to visualize the interconnectedness of the current AI investment ecosystem.

Yes, there are risks. We will highlight a few risks to the AI thesis below, but not with the intention of deterring investment. Instead, we view our role as risk managers, seeking to manage exposures appropriately and maintain sufficient portfolio diversification. So what should investors be looking at today?

Risk #1: Valuations. Lately the investment mantra has been “BUY BUY BUY!” The S&P 500 today trades are 22.8x forward earnings, about 34% higher than the 30-year average. Not only that, but the top 10 stocks trade at a remarkable 40% of the index and an average multiple of 29x next year’s earnings. The S&P 500 today has a strong correlation to expensive technology and growth stocks, a risk many investors may not consider.

Risk #2: Economic Breadth. The underlying economy still matters! Consumers still need to spend money in order for Apple or Tesla to make money. Advertisers need to pay for the eyeballs and clicks on Facebook and Google. If the economy begins to contract, would that mean the hyperscalers are forced to slow down investment and the AI trade begins to crumble? Positive growth is still expected this year at around 1.6% GDP. Will this be enough to sustain the AI momentum?

Risk #3: Competition. In the US alone, there are currently over 1000 LLMs available to the public. OpenAI recently announced a partnership with AMD – a strong indication that other semi-conductor companies are capturing part of the AI infrastructure. Regulation may also impact the competitive landscape. China is building its own AI ecosystem, and it is in periods of technological expansion that new market leaders emerge. Will any of the Magnificent 7 have their market position supplanted by an AI upstart? Time will tell.

Cutler Market Positioning

The S&P 500 rallied 8.12% in the third quarter, leading to a year-to-date return of 14.83%. Despite the strong AI rally and investment cycle outlined above, nearly every asset class has seen year-to-date gains. Gold has been a standout, and while the historical returns of gold versus stocks is less compelling, the long-term trend has been upended in 2025. Uncertainty and global central banks diversifying their holdings from the US dollar has led to gold recently breaching the $4000/ounce level, up over 50% this year. Should the dollar continue to fall this may further contribute to gold’s ascension, but we would rather participate in that trend through ownership of foreign equities. Through September 30th, Emerging Market stocks had rallied an impressive 28%, with Developed Market stocks (think European, Japanese, and Australian equities) up over 25%.

However, our most actionable advice is also admittedly the most self-serving; Cutler’s long-held philosophy of buying quality and income. Many investors remember previous “market bubbles” and harken back to the technology bubble in the late 1990’s. We believe an important lesson from that era is that much of the market gains occurred after Alan Greenspan warned of “irrational exuberance” in December of 1996. In fact, the NASDAQ didn’t peak until March of 2000- about 3 ½ years later! Learning that lesson, we continue to encourage participation in equities. However, our advice is not to “chase” performance. While the Magnificent 7 stocks trade at nearly 30 times next year’s earnings, the rest of the market looks attractive at are more reasonable 19.5 times earnings. And with a growing economy and interest rates on a path lower, this valuation appears reasonable.

Our advice remains to stay diversified. Dividend stocks (and value stocks) remain an attractive opportunity as the benefits of AI begin to spread to other industries. International equities continue to have a lower-dollar tailwind. And growth stocks, which have carried the day for US investors, should continue to be a part of investor portfolios. Rebalancing can help to mitigate risks, and bonds should hold value as the Fed lowers rates.

Past performance is not indicative of future results. Strategies referenced herein may be materially different than actual positions held in client accounts. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be profitable or suitable for a particular investor's financial situation or risk tolerance. Investing involves risk, including loss of principal. You cannot invest directly in an index. Nothing herein should be considered a recommendation to buy or sell a security, including any securities, mutual funds, or ETFs specifically provided as examples. Asset allocation and portfolio diversification cannot assure or guarantee better performance and cannot eliminate the risk of investment losses. Neither Cutler Investment Counsel, LLC nor its information providers are responsible for any damages or losses arising from any use of this information.

The S&P 500 Index is widely regarded as the best single gauge of large-cap U.S. equities. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

The Barclay’s Aggregate Bond Index (Taxable Bond) is a broad base, market capitalization weighted bond market index representing intermediate term investment grade bonds traded in the United States.

Headline Inflation is the raw inflation figure reported through the Consumer Price Index (CPI) that is released monthly by the Bureau of Labor Statistics.

The Bloomberg Commodity Index (Commodities) is an index of the prices of items such as wheat, corn, soybeans, coffee, sugar, cocoa, hogs, cotton, cattle, oil, natural gas, aluminum, copper, lead, nickel, zinc, gold and silver. The index is calculated on an excess return basis and reflects commodity futures price movements.

The MSCI EAFE Index (Foreign Developed Index) is designed to represent the performance of large and mid-cap securities across 21 developed markets, including countries in Europe, Australasia and the Far East, excluding the U.S. and Canada.

The MSCI Emerging Markets Index captures large and mid-cap representation across 27 Emerging Markets (EM) countries. With 1,392 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Bitcoin Each crypto index is made up of a selection of cryptocurrencies, grouped together and weighted by market capitalization (market cap). The market cap of a cryptocurrency is calculated by multiplying the number of units of a specific coin by its current market value against the US dollar.

Source: Morningstar All opinions and data included in this commentary are as of September 30, 2025 and are subject to change. The opinions and views expressed herein are of Cutler Investment Counsel, LLC and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This report is provided for informational purposes only and should not be considered a recommendation or solicitation to purchase securities. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed.

Tags: global market, volatility, financial planning, gifting, taxation

CATEGORIES

Disclaimer

These blogs are provided for informational purposes only and represent Cutler Investment Group’s (“Cutler”) views as of the date of posting. Such views are subject to change at any point without notice. The information in the blogs should not be considered investment advice or a recommendation to buy or sell any types of securities. Some of the information provided has been obtained from third party sources believed to be reliable but such information is not guaranteed. Cutler has not taken into account the investment objectives, financial situation or particular needs of any individual investor. There is a risk of loss from an investment in securities, including the risk of loss of principal. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable or suitable for a particular investor's financial situation or risk tolerance. Any forward looking statements or forecasts are based on assumptions and actual results are expected to vary. No reliance should be placed on, and no guarantee should be assumed from, any such statements or forecasts when making any investment decision.